Current News in Oil, Gas, and Energy as of 1 March 2026: Geopolitical Risk Premium in Oil, OPEC+ Production Decision, Gas and LNG Market Situation in Europe, Coal Dynamics in Asia, Refinery Margins and Prospects for Renewable Energy. Analysis for Investors and Participants in the Global Energy Sector

The global energy sector enters March with heightened volatility: geopolitical tensions surrounding Iran once again generate a “risk premium” in oil prices, while OPEC+ participants will determine production parameters for April in the coming hours. The European gas market remains tense due to low storage levels and high sensitivity to weather conditions and LNG logistics. At the same time, coal continues to underpin energy security in Asia, and oil products and refineries are assessing margin prospects amidst fluctuations in raw material prices.

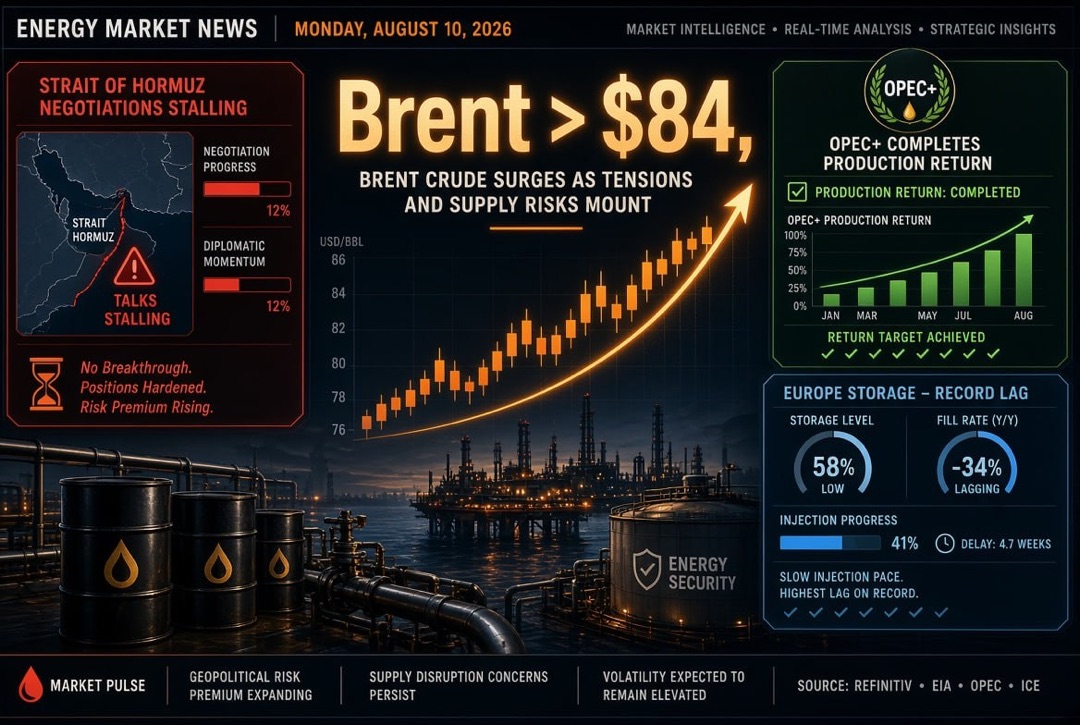

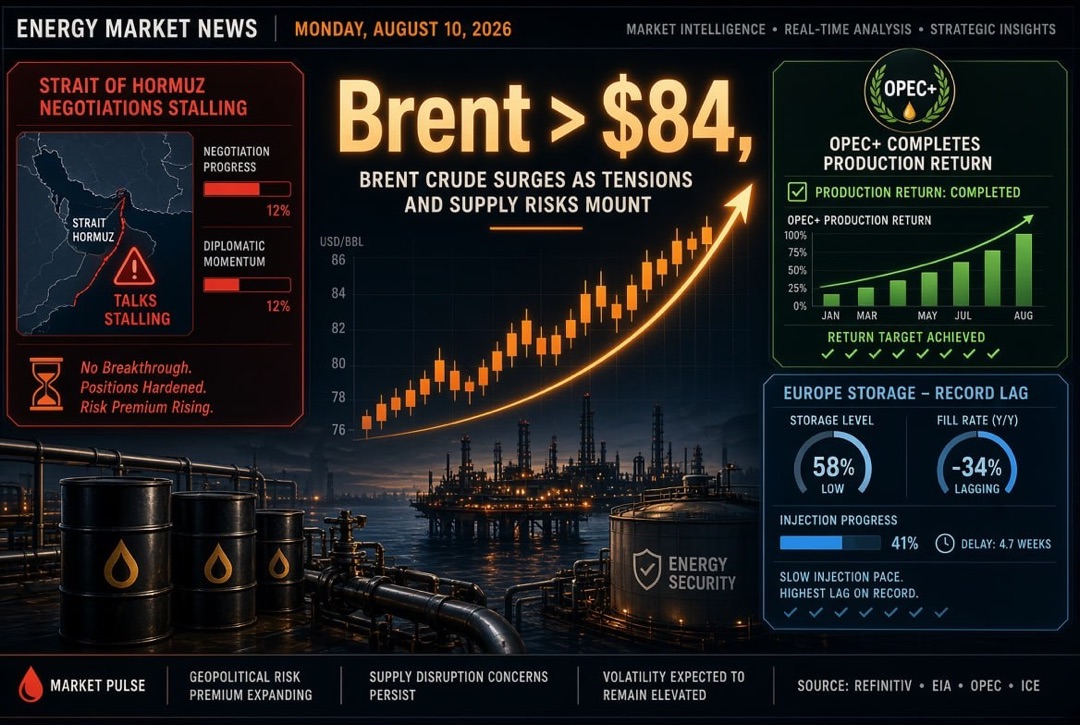

Oil: Risk Premium and Scenarios for the Strait of Hormuz

A key driver of today’s agenda is the rising geopolitical risks in the Middle East. For global investors, this means an expanded range of expectations for Brent and WTI, as the market rapidly reassesses the likelihood of supply disruptions and hedges risks through a premium on price. The most sensitive point is the Strait of Hormuz, through which a significant share of global maritime oil and petroleum trade passes.

- Base Scenario: Tensions remain high, but without sustained physical supply disruptions—oil maintains a “risk premium,” and volatility is elevated.

- Negative Scenario: Local disruptions or shipping restrictions—Brent quickly tests higher levels, and market participants price in shortages on a weekly horizon.

- Positive Scenario: De-escalation—premium decreases, attention returns to supply-demand balance and expectations of seasonal surplus.

OPEC+: Decision on 1 March and Dilemma Over Production

Today’s meeting of key OPEC+ participants essentially sets the “tuning” of the market for April: either a confirmation of the previously expected moderate increase in production or a more significant adjustment aimed at stabilising the market amid rising risks. For investors in oil and gas and participants in the oil market, this is more important than short-term price fluctuations: production parameters determine the physical flow of barrels and signal for the forward curve.

Factors that will determine the final decision include:

- Geopolitics and Supply Disruption Fears: necessity to mitigate the risk of shortages in the event of deteriorating conditions.

- Seasonal Demand: the transition to spring is often accompanied by weaker demand for petroleum products in certain regions.

- Inventories and Discipline: the market closely monitors quota compliance and actual deliveries.

Oil Products and Refineries: Margin Under Pressure from Volatility

For the oil products and refinery segment, the current situation entails an increase in price risk for raw materials amid uneven demand for end products. The fuel market typically reacts with a lag: raw materials rise in price faster than refining can pass the increases onto gasoline, diesel, and jet fuel. In such conditions, inventory management and hedging become crucial.

Key focus areas for downstream participants include:

- Crack Spread: a measure of refinery margins for gasoline and diesel—a gauge of refinery resilience during oil price spikes.

- Logistics and Freight: escalating geopolitical risks may increase transportation and insurance costs.

- Regional Demand: Europe and Asia are entering the season differently, affecting product premiums.

Gas and LNG: Europe Maintains Focus on Storage and Supply Costs

The European gas market is concluding winter with heightened sensitivity to news regarding storage levels, weather, and global competition for LNG cargoes. Prices in Europe remain at levels where market participants are closely evaluating injection rates in spring and the system’s ability to navigate the next heating season without stress scenarios.

A particular risk for gas and LNG is any events affecting logistics and the insurance of supplies through key maritime routes. Under stress scenarios, even short-term restrictions can lead to price spikes, as the market reacts to the scarcity of “flexible” volumes.

Electricity and Renewable Energy: Balancing Reliability and Capital Costs

In the electricity sector, including renewable energy, the main theme revolves around capital costs and the reliability of energy systems. High fuel volatility increases the value of stable generation and flexibility (dispatchability, balancing, storage), but simultaneously impacts capital expenditure and payback periods for projects. For investors, this indicates that models minimizing fuel price risk through contracts, while maintaining income supported by predictable demand, will prevail.

- Renewable Energy: sensitive to financing costs and equipment supply chains.

- Gas Generation: benefits as balancing power but depends on gas prices and LNG availability.

- Grid Infrastructure: investments in grid and dispatching become critical for the integration of renewable energy.

Coal: Asia Maintains Demand, Market Assesses Import Substitution

The coal segment remains essential for energy security in Asia. Supply and inventory levels in key regions sustain attention on thermal coal prices, particularly against the backdrop of certain countries’ plans to reduce imports while simultaneously boosting domestic generation. For the global energy sector, this means sustained demand for coal as a “security” fuel, despite the long-term trend of energy transition.

The practical logic of the coal market today includes:

- If inventories are below normal—prices react swiftly to any news regarding logistics and demand.

- If imports are restricted by policy—domestic production and coal quality become more significant.

- If new capacities are coming online—base demand for thermal coal increases.

Market Geography: Middle East, Europe, Asia, USA

The Middle East sets the “upper boundary” of risks through geopolitics and maritime logistics. Europe continues to restructure its gas balance, maintaining focus on LNG and storage. Asia remains a key demand centre for coal and a driver of overall energy consumption growth. The USA influences through oil and gas production, financial conditions, and inflation expectations, which in turn set capital costs for energy projects.

Implications for Investors and Energy Sector Participants

In the coming days, the outcomes of the OPEC+ decision and the evolving situation surrounding Iran will be key, as these will define the short-term price corridor for oil and volatility in related markets. For companies in the energy sector, refineries, and traders, it is essential to combine operational discipline and risk management: the period of “jagged” prices enhances the value of flexibility and access to logistics.

- Oil and Oil Products: preparedness for a wide price range; inventory control; margin hedging.

- Gas and LNG: monitoring of European storage levels and competition for cargoes; assessment of stress supply routes.

- Electricity and Renewable Energy: focus on financing costs and cash flow sustainability.

- Coal: tracking import policies in Asia and inventory dynamics as leading indicators for price.

Upcoming Triggers Calendar

The commodity and energy market enters March with high news sensitivity. Participants in the energy sector should keep an eye on the following triggers:

- OPEC+ decision on production for April and subsequent comments on market balance;

- Dynamics of risks in the Strait of Hormuz region and their impact on freight/insurance;

- European gas storage levels, injection rates, and price expectations for spring;

- Signals from Asia regarding coal and electricity (imports, new capacities, demand).

Conclusion: The global energy sector begins March with a predominance of geopolitics in oil and increased vulnerability of the European gas market. In such an environment, strategies that combine raw material diversification (oil, gas, coal), resilient logistics, and stringent risk control over refining margins and supply contracts will prevail.