Global Energy Market News as of 4 March 2026: Rise in Brent and WTI Oil Prices, Surge in European Gas and LNG, Supply Risks through the Strait of Hormuz, Dynamics of Oil Products, Refineries, Electricity, Renewables and Coal, Analysis for Investors and Participants in the Global Energy Market

Key Market Figures for Oil, Gas and Energy

Below are the benchmarks that are shaping the "pricing of risk" for oil, gas, electricity and oil products as we head into Wednesday. These levels are significant for assessing margins, hedging and stress scenarios in supply chains.

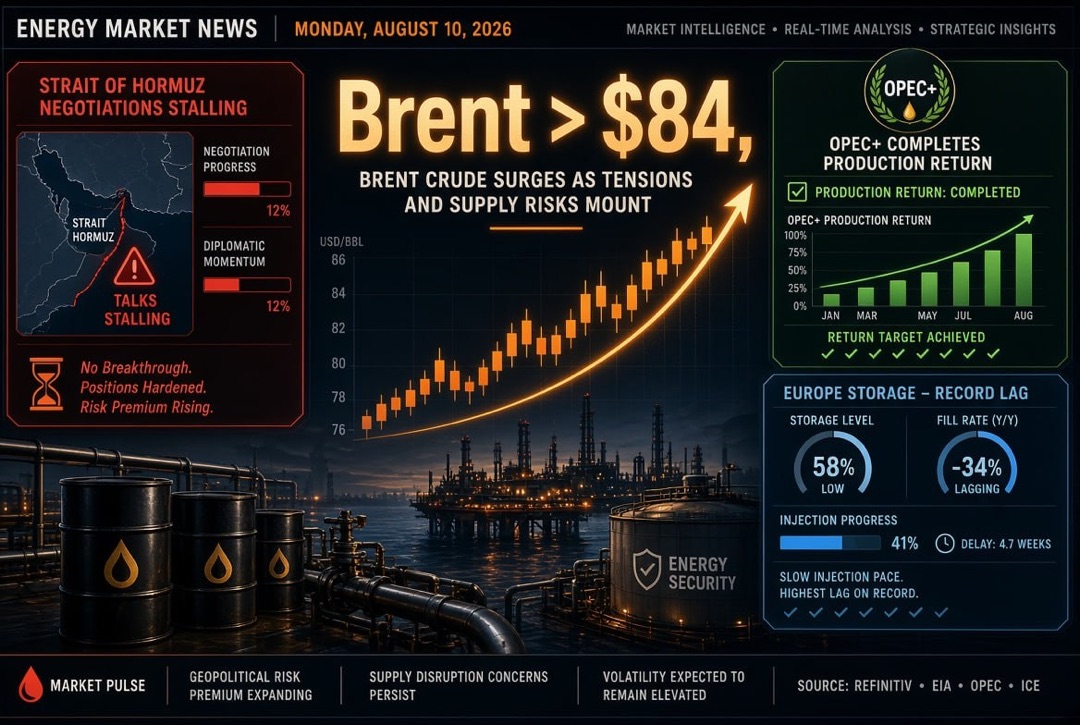

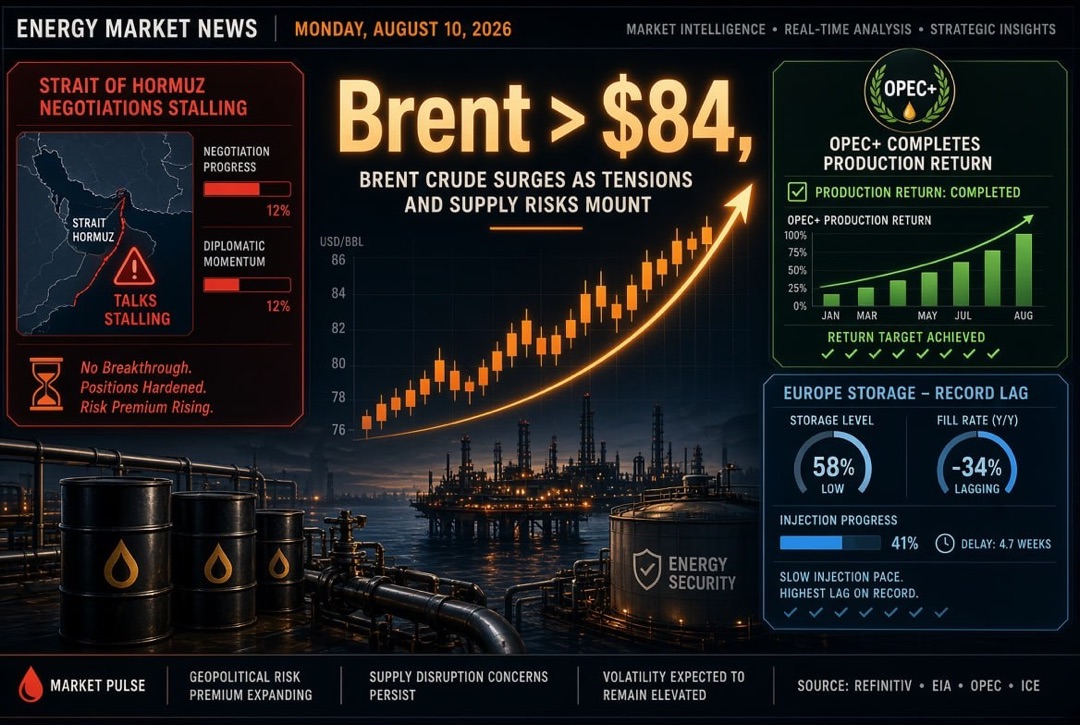

- Oil (Brent/WTI): The market has factored in a sharp risk premium due to potential disruptions; Brent and WTI quotes have fluctuated dramatically in recent sessions, testing multi-month highs.

- Gas (Europe, TTF): European gas prices have shown one of the strongest price surges in a short period since the crisis years, raising expectations for an increase in electricity and heat generation costs.

- LNG (JKM, Asia): Asian LNG indicators have risen in response to supply risks and increased freight costs; this indicates a rise in "last mile" costs for importers.

- LNG Freight: LNG shipping rates have surged, placing a direct strain on spot purchase economics and trader portfolio flexibility.

- Coal: Thermal coal and coal generation are once again viewed by parts of the market as a "hedge" against expensive gas, particularly in countries where quick shifts in generation are possible.

- Carbon Regulation (EU ETS): Carbon prices in Europe remain a standalone factor for power generation and energy-intensive sectors, but during crisis periods they are temporarily overshadowed by gas.

Oil: Geopolitical Premiums, OPEC+ and Supply Routes

The primary driver is the risk of physical supply reductions through a critical point in global energy logistics. In oil markets, this is quickly reflected in rising "risk premiums" and the re-evaluation of barrel availability in the short term. An important point for investors: even when formal inventories are available to consumers, a short-term shortage of tankers, insurance coverage, and safe routes can sharply increase the cost of delivery "here and now."

Moreover, the OPEC+ decision to gradually adjust production (scheduled increase next month) is perceived by the market as a secondary factor against the backdrop of a logistical disruption threat. The key question remains—how many "real" barrels can quickly enter the market and through what routes, should tensions persist? An additional layer of uncertainty is the ability of individual producers to redirect exports to alternative terminals and pipeline corridors: the cost of such a reconfiguration is high and limited by infrastructure capacity.

Asia warrants particular attention: China, as the largest oil importer, is already beginning to adapt at the refining level—history shows that a decrease in throughput at sensitive refineries can act as a rapid "valve" for balancing the domestic raw material market and reducing supply deficit risks. For the global market, this indicates a potential redistribution of demand for spot cargoes and shifts in premiums/discounts across grades.

In the United States, the focus is on policies to mitigate price shocks for consumers. The Strategic Petroleum Reserve (SPR) factor remains a tool, but markets will assess not just statements, but actual intervention readiness and its scale. For institutional investors, it is crucial to note: even without an immediate release of oil from reserves, the mere signal of a possible reaction can impact the futures curve and volatility.

Gas and LNG: Europe and Asia Compete for Molecules Again

The main gas shock relates not only to the price of the raw material but also to the "quality of availability" of supplies. A halt in LNG production at one of the key export hubs has instantly heightened competition between Europe and Asia for alternative marine volumes. In Europe, this issue appears especially sensitive due to the fact that storage levels are below typical values as we enter the refilling season—this increases the likelihood of aggressive purchasing as early as spring, despite the traditional "shoulder" season.

Asia is pragmatically reacting: importers are evaluating which volumes can be secured through long-term contracts and which will need to be purchased on the spot market at considerably higher prices. For India, the risk is most direct—there are already indications of countermeasures concerning gas distribution and preparations for spot tenders. In Japan, the focus is shifting towards inventory management and coordination among companies, including the use of internal mechanisms to redistribute LNG shipments. For the market as a whole, this signifies a growing "value of flexibility": portfolios with access to American LNG and available volumes are becoming strategic assets.

A separate factor is freight and insurance. Even if gas is physically accessible, delivery costs and insurance limitations can render spot purchases economically unviable for some buyers. This raises the risk that poorer importers will be pushed out of the market, exacerbating socio-political risks and increasing the likelihood of regulatory interventions in certain countries.

Oil Products and Refineries: Diesel, Jet Fuel, and Gasoline Prices Rise Faster than Oil

Oil product markets typically react more sharply to logistics disruptions than the crude oil market. The reason is straightforward: products represent the "final stage" of the chain, meaning their sensitivity to refinery issues, supply routes, and regional deficits is heightened. Diesel and jet fuel take centre stage—critical fuels for industry, logistics, and aviation, where rapid substitutions are limited.

Already, increases in premiums and spreads between regions are evident: Europe is structurally vulnerable concerning diesel and, in the event of prolonged restrictions, may increasingly "pull" shipments from Asia, changing traditional trade flows through Singapore and Northeast Asia. For traders, this means expanded arbitrage opportunities but also an increase in operational risks (vessel timing, fleet availability, insurance, counterparty limits).

A second layer of risk involves potential shutdowns and maintenance at refineries. Any unplanned processing losses in the Middle East or other regions, along with seasonal repair boosts in Europe and Asia, increase the likelihood of a "product" shock, even if the physical oil deficit turns out to be less dramatic. For fuel companies, this signals a need to reassess inventories, supply logistics, and pricing strategies.

Electricity and Renewables: Network Resilience Becomes a Pricing Factor

The gas surge inevitably translates into electricity costs in regions where gas remains the marginal fuel. Consequently, markets are increasingly evaluating not only the availability of gas but also the energy system's capacity to smooth out short-term peaks—through renewables, energy storage, and grid infrastructure.

In Europe, interest in scaling up energy storage projects is accelerating: battery projects are becoming tools for both renewable integration and managing price extremes (shifting consumption/production over time). For investors, this confirms the thesis that the "energy transition" encompasses not only generation (wind/solar) but also balancing infrastructure. Simultaneously, in Asia, the role of dispatch and reserves is strengthening, while in China, the development of trunk networks and high-voltage transmission remains a cornerstone for long-term energy consumption expansion and resource transfer across regions.

Coal and Nuclear: Alternatives Amidst Expensive Gas

When gas and LNG prices rise sharply, coal generation often temporarily regains attractiveness—primarily in countries where coal infrastructure is maintained and where switching between fuels can occur without extensive investments. In the short term, this could support coal indices and freight, as well as increase demand for low-sulphur grades in Asia. Notably, some of the largest systems (including China) maintain domestic production and managed imports, reducing vulnerability to sharp fluctuations in global prices.

Concurrently, within the "alternative" fuel sector, nuclear generation remains pertinent: amid recurring energy stresses, regulators and large consumers are increasingly interested in reliable low-carbon baseload power. The uranium market, while a separate story, could serve as a marker of sustained political demand for nuclear projects and fuel cycles in long-term portfolios (energy/infrastructure).

What Investors and Energy Companies Should Monitor on 4 March

On Wednesday, the focus shifts from "shock news" to assessing market resilience: will logistical constraints be confirmed, will alternative routes emerge, and how quickly will consumers adapt demand and inventories? For the oil, gas, electricity, and oil products markets, the key triggers can be summarised in the following short checklist.

- Statistics and Inventories: weekly data on oil and oil products in the US (as a signal for demand and refinery throughput), as well as commentary from regulators and industry associations.

- Shipping and Insurance: trends in tanker and LNG vessel passages, availability of insurance coverage, rising freight rates, vessel queues, and unloading delay risks.

- Oil Products: diesel and jet fuel spreads between regions, changes in premiums in Asia and Europe, signs of shortage formation in specific hubs.

- European Gas and Storage: pace of storage replenishment, demand reduction measures, and competition for LNG cargoes.

- Corporate News: updates from major producers, refineries, and traders regarding redirection of flows, force majeure events, maintenance, and terminal availability.

A fundamental takeaway for investors: in the upcoming sessions, energy market participants will reward not so much a "directional bet," but the quality of risk management—through diversification, hedging, liquidity control, and assessment of secondary effects (oil products, electricity, freight, insurance). In such an environment, companies with flexible supply portfolios, strong logistics, and access to alternative raw material and LNG markets stand to benefit.