Startup and Venture Investment News for Monday, 29 June 2026: Growth in AI Infrastructure, Major Venture Rounds, IPO Window, China, India, Deeptech, and Key Signals for Investors

The global venture market enters the last week of June 2026 in a state of robust but increasingly uneven recovery. Startups related to artificial intelligence, computing infrastructure, robotics, space technologies, and semiconductors continue to attract the lion's share of capital. At the same time, investors are increasingly questioning not whether there is growth, but rather how sustainable current valuations are and where the line is drawn between technological breakthroughs and new investment bubbles.

For venture funds, family offices, and institutional investors, the key theme for Monday, 29 June 2026, is the concentration of capital in AI infrastructure and growing demand for liquidity through IPOs. Following a record first quarter, significant AI rounds, and a revival in public offerings, the market remains open for strong companies but is becoming considerably more demanding regarding unit economics, revenue quality, and startups' ability to convert technological excitement into sustainable profit.

Venture Market: Capital Has Returned, But Is Distributed Extremely Selectively

The primary trend of 2026 is the return of significant capital to venture investments, albeit not in the previous broad format. In past cycles, money was distributed across a multitude of industries, whereas now a considerable portion of financing is concentrated around a limited array of sectors: artificial intelligence, AI infrastructure, robotics, defence technologies, space, chips, and enterprise software.

According to sector estimates, global venture financing reached record levels in the first quarter of 2026, with AI startups emerging as the leading recipients of capital. This indicates that the venture market has formally recovered, but the recovery is asymmetric: the strongest companies are securing mega-rounds, while startups without a clear technological advantage, revenue, or strategic buyers are facing tougher negotiations.

- Growth funds are more actively entering late stages if they see the prospect of an IPO or strategic sale.

- Seed and Series A investors are more cautious in assessing projects without proven monetisation.

- Corporate investors are intensifying their interest in startups that can close technological gaps in AI, cybersecurity, and manufacturing.

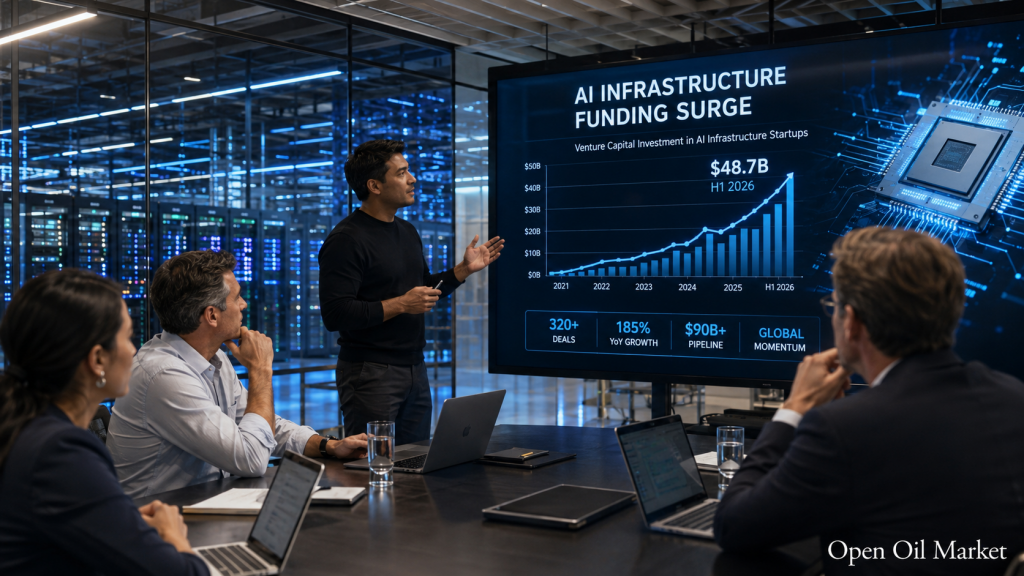

AI Infrastructure Remains a Magnet for Venture Capital

Artificial intelligence continues to be the primary driver of venture investments, but the market's focus is gradually shifting from universal models to infrastructure. Investors are looking for companies that generate revenue through computational capabilities, optimising inference, data centres, network infrastructure, data storage, tools for AI agents, and corporate security.

A notable event in June has been the interest in Baseten — an AI infrastructure company in the inference segment. The startup is reportedly close to raising a substantial round with a valuation of up to $13 billion, underscoring the scale of demand for solutions that allow companies to launch AI products faster and more cost-effectively. At the same time, this example highlights the risk of overheating: the valuations of such companies are rising faster than the market can verify the sustainability of their revenues.

This poses a new dilemma for venture investors. On one hand, AI infrastructure is becoming analogous to the "energy system" of the digital economy. On the other hand, excessive competition for the best deals leads to complex round structures, differing entry prices for investors, and heightened expectations for future growth.

New Unicorns: India, the USA, and Global Competition for AI Sovereignty

One of the significant international signals remains the rise of national AI champions. The Indian company Sarvam raised $234 million at a valuation of around $1.5 billion, becoming a new AI unicorn. For the market, this is not merely another substantial round but a confirmation of a broader trend: governments and large corporations are eager to control critically important AI technologies, language models, computing power, and local data.

Venture investments are increasingly intersecting with industrial policy. Startups in AI, robotics, semiconductors, and space technologies gain advantages not only through their products but also due to their strategic significance for national economies.

- India is strengthening its position in applied AI and local language models.

- The USA retains leadership in frontier AI, infrastructure, and large private technology companies.

- China is accelerating support for AI, chips, robotics, and "industries of the future."

- Europe is betting on industrial AI, regulation, and deeptech.

The Chinese Venture Market: "Industries of the Future" and Bubble Risk

China is becoming one of the most active regions in the venture market in June 2026. Support for startups in strategic sectors — space, quantum technologies, nuclear fusion, robotics, semiconductors, AI, and brain-computer interfaces — has led to a sharp increase in fund activity. Private equity and venture capital investments in China grew by nearly 60% in the first five months of the year, and new venture funds have already attracted more capital than in the entire previous year.

For global investors, this presents a dual signal. On one hand, the Chinese market is once again offering large-scale opportunities for investments in deeptech and industrial innovations. On the other, the rapid growth in valuations creates a risk of overheating, particularly in companies without revenue, where the investment narrative is based on future government contracts, technological promises, and anticipated IPOs.

Among the most interesting areas for funds are:

- commercial space and satellite infrastructure;

- robotics and embodied AI;

- memory chips and specialised AI processors;

- quantum technologies and photonic computing;

- manufacturing startups for AI servers and data centres.

IPO Window: The Public Market is Once Again Important for Venture Exits

The revival of IPOs remains the second most significant factor after the AI boom. Venture funds have been waiting for liquidity recovery for several years, and now the public market is once again becoming a viable exit channel. The success of major technology and infrastructure placements creates a benchmark for private companies, but investors are no longer prepared to buy any growth without analysing profitability.

Lime, backed by Uber, is preparing for an IPO in the USA with a valuation of up to $1.66 billion. The company operates in 230 cities across 29 countries but remains an example of a complex consumer startup: there is scale, there is revenue, yet the business relies on seasonality, regulation, asset costs, and city permits. Therefore, Lime's placement will serve as an important test of demand for startups beyond the AI sector.

Particular attention is drawn to OpenAI: the company, according to market reports, may postpone its public debut until next year. This is an important signal for the entire industry. Even the largest AI companies are keen to choose the timing of their public offerings carefully to avoid entering a window of high volatility and securing valuations before completing the next growth phase.

M&A and Strategic Investments: Corporations are Buying Technologies, Not Just Revenue

In the context of high valuations and a lack of liquidity, M&A deals are becoming an increasingly important tool for the venture ecosystem. Large technology companies, industrial groups, and defence corporations are looking at startups as a means to quickly access technologies, teams, and intellectual property.

The most likely areas of consolidation in the second half of 2026 include:

- AI infrastructure — acquisitions of companies that reduce the cost of computations and inference.

- Cybersecurity — deals focused on protecting AI agents, data, and corporate perimeters.

- Industrial AI — integration of startups into energy, manufacturing, logistics, and defence sectors.

- Fintech — consolidation of payment, credit, and B2B services.

- Space and robotics — acquisitions of teams with unique engineering competencies.

Europe and Emerging Markets: A Focus on Industrial AI and Local Champions

The European venture market is showing more moderate dynamics than the USA and China, but its structure is becoming qualitatively more interesting. Here, greater attention is given to industrial AI, robotics, climate technologies, energy, cybersecurity, and enterprise software. For funds, this is a less speculative but potentially more sustainable model: startups are more frequently selling solutions to corporate clients and integrating into real production chains.

Emerging markets are also becoming more prominent. India is strengthening its position in AI and fintech, Southeast Asia is attracting capital in digital commerce, B2B services, and customer communication automation, while the Middle East continues to leverage sovereign capital to create technology hubs. For venture investors, this means an expansion of deal geography but also requires a deeper analysis of currency risks, regulation, and the quality of local exits.

What is Important for Venture Investors and Funds on 29 June 2026

Monday, 29 June 2026, opens a week in which investors will evaluate not only news about new rounds but also the resilience of the entire venture construct. The startup market is active again, yet money is concentrating in the hands of a limited number of companies and sectors. This heightens competition for the best assets while simultaneously increasing the risk of misjudgment in valuations.

For funds, key landmarks remain:

- Revenue quality — recurring revenue, long-term contracts, and proven monetisation are more important than presentation growth.

- Cost of computations — for AI startups, it is crucial to understand how margins change when scaling.

- Path to liquidity — IPOs and M&A are operational again, but the public market requires financial discipline.

- Regulatory resilience — particularly in AI, fintech, robotics, defence technologies, and data.

- Geopolitical factor — investments in deeptech increasingly depend on national strategies and cross-border capital restrictions.

The overall picture for the global startup ecosystem remains positive yet ambiguous. Venture investments are rising again, AI infrastructure is shaping new mega-valuations, the IPO market is reviving, and emerging regions are receiving more attention. However, now it is crucial for investors to maintain discipline: in this new phase of the market, success will not belong to those who merely ride the hype surrounding artificial intelligence, but to those who can distinguish the infrastructural platforms of the future from overvalued companies reliant on short-term investment enthusiasm.