Current Updates in the Oil, Gas, and Energy Sector as of 3 March 2026: Geopolitical Risks Surrounding the Strait of Hormuz, Oil and Gas Volatility, LNG Dynamics, Refinery Margins, Electricity, and Renewable Energy – A Global Overview for Investors and Energy Companies

As March begins, the energy markets are experiencing heightened turbulence: geopolitical events in the Middle East have amplified concerns regarding oil and gas supplies, and the risk of logistical disruptions in the Strait of Hormuz has emerged as a key topic for investors, traders, and fuel companies. Against this backdrop, volatility has surged across the oil, gas, LNG, petroleum products, and electricity segments, prompting market participants to swiftly reassess scenarios related to inflation, refinery margins, and supply chain resilience.

Oil: Geopolitical Premium and Surge in Volatility

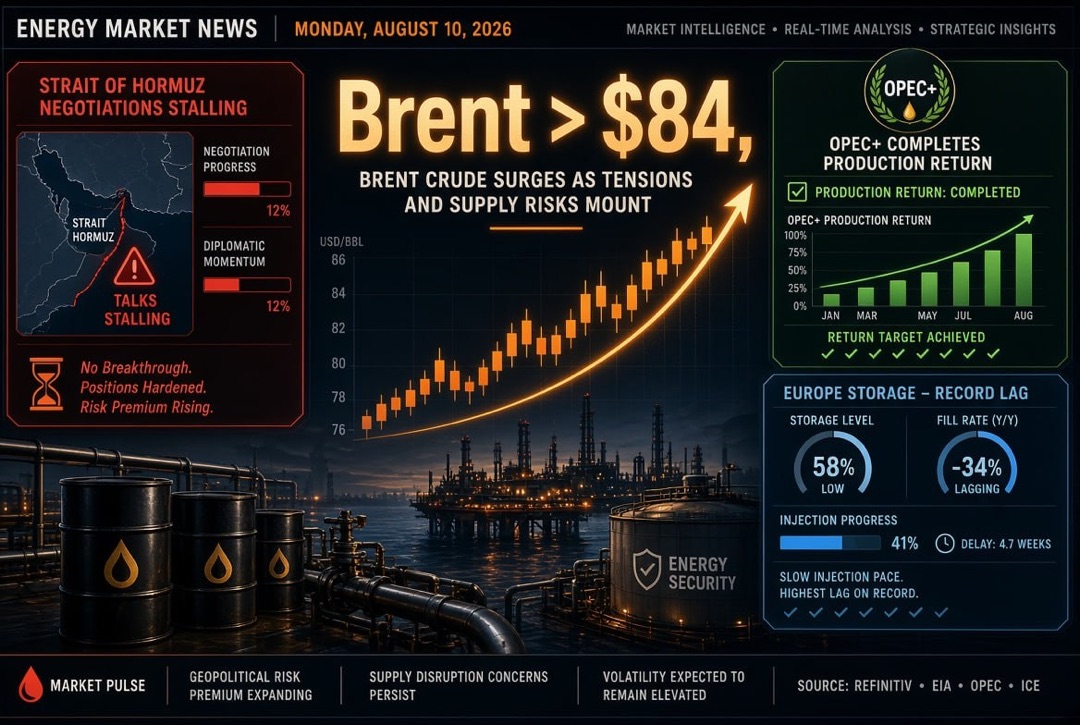

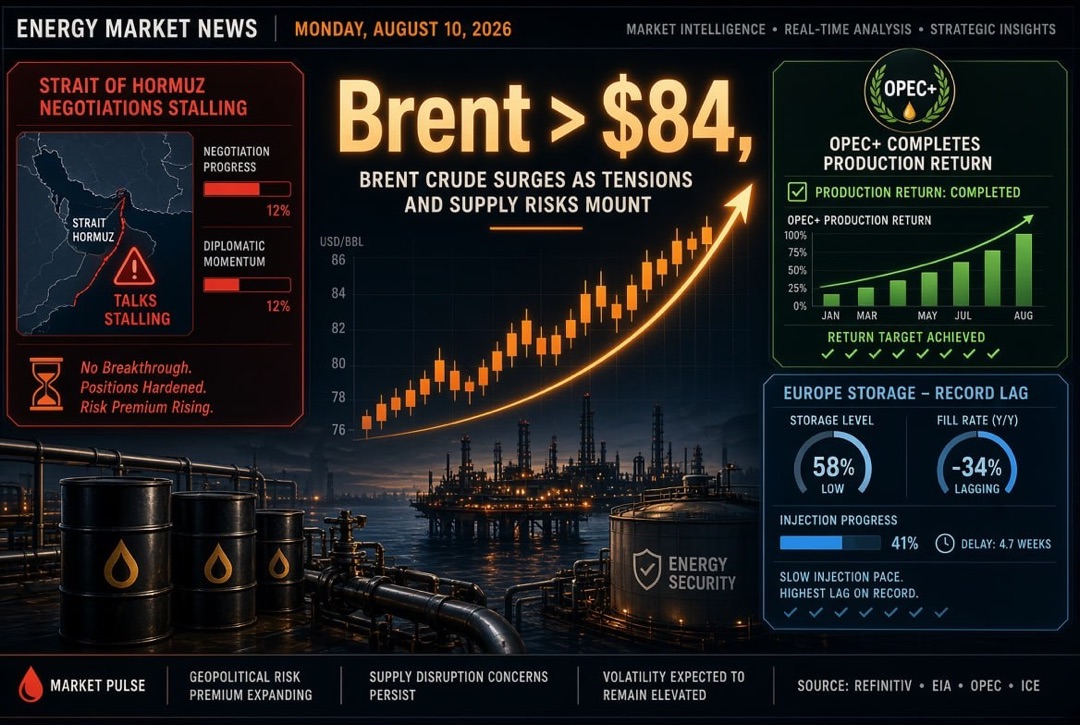

Oil prices have received a sharp impetus from the geopolitical premium: the market is pricing in the likelihood of production and export disruptions in the Persian Gulf region, as well as risks to shipping. The focus is not so much on the current demand-supply balance but rather on the “tail risks” (low probability but high impact) should the conflict escalate and tanker movements be restricted.

- Brent and WTI reacted with a rapid increase to news concerning risks to infrastructure and logistics; subsequently, part of this movement was corrected as profits were realised.

- Spreads on grades and differentials have intensified sensitivity to the availability of “free barrels” in the Atlantic and Asia.

- The rise in oil prices is reflected in inflation expectations and fuel costs, which are significant for the transport sector and petrochemicals.

The Strait of Hormuz and Maritime Logistics: A Principal Systemic Risk for the Energy Market

The Strait of Hormuz remains a strategic artery for global oil and petroleum product trade, as well as for LNG supplies from the region. Even temporary restrictions on movement lead to increased insurance premiums, rising freight costs, and the formation of a “logistical shortage”, where the physical resource is available but more challenging and expensive to transport.

Changes for Market Participants

- Increased freight and insurance rates for tankers and gas carriers.

- Flow rotations: heightened significance of alternative routes and redirection of supplies depending on regional market premiums.

- Increased demand for storage capacities and commercial reserves as a hedging tool for supplies.

OPEC+ and Production: Quota Policies under Market Stress

On the supply side, the reaction of OPEC+ countries and the largest producers outside the cartel is crucial. The market is assessing the extent to which current quota decisions and voluntary restrictions can offset potential supply disruptions should the risk transition from an “informational” to a “physical” format.

Key Decision Points

- Baseline Scenario: maintaining the current production trajectory with targeted adjustments and signals of readiness to stabilise the market.

- Stress Scenario: expedited decisions for increased production by individual participants if physical oil flows are disrupted.

- Stabilisation Scenario: easing of the geopolitical premium and a return of focus to demand, inventories, and macroeconomics.

Gas and LNG: Capacity Downtimes and Price Shocks in the Spot Market

The gas and LNG segments have emerged as the primary source of price momentum at the beginning of March. The market is reacting sharply to reports of risks and downtimes at major export facilities: global LNG trade is more concentrated, and “quick replacements” for lost volumes are fewer than in oil. Europe is concurrently competing for LNG with Asia, and during periods of stress, this competition intensifies.

- European gas benchmarks experienced a sharp upward movement amid the threat of production cuts and rising risk premiums.

- Asian LNG indices also saw gains, reflecting expectations of rising prices for spot cargoes and extended delivery times.

- For importers (energy companies and industry), the focus is on hedging costs and availability of short-term volumes.

Risks for Europe and Asia

- Europe: sensitivity to inventory levels and the pace of storage replenishment, increased “weather premium” during cold anomalies.

- Asia: price competition for spot, especially among countries with a high share of LNG in their electricity balances.

Refineries and Petroleum Products: Margins, Diesel, and Consumer Demand Response

For the refinery and petroleum products segment, a critical combination of factors is at play: rising raw material costs (oil), changes in logistics, and seasonal demand profiles for gasoline, diesel, and jet fuel. In the context of sharp movements in oil prices, “crack spreads” may behave inconsistently: some markets gain support due to delivery risks, while others face pressure due to declining demand and rising prices for consumers.

Monitoring for Fuel and Oil Companies

- Dynamics of refining margins and differentials for regions Europe—Asia—USA.

- Status of diesel and jet fuel inventories, sensitive to logistical disruptions.

- Risk of a “disconnect” between market prices and physical premiums in ports.

Coal: Asia and Energy Security

The coal market frequently experiences additional demand from generation during gas stress periods, especially where fuel switchability is retained. However, the price trajectory of coal depends on the availability of logistics, decarbonisation policies, and competition with gas and renewable energy in the electricity sector. For energy companies, coal remains a “insurance” element against expensive gas, but regulatory and ESG constraints continue to narrow the horizons for long-term investments.

Electricity: The Impact of Gas, Industrial Risks, and Grid Security

The electricity segment directly responds to the costs of gas and coal as well as to the availability of capacity during peak hours. Rising gas quotations increase the marginal costs of generation in systems where gas determines prices in power/electricity markets. For industries, this entails rising operational costs; for energy companies, it necessitates heightened requirements for risk management and liquidity.

Short Checklist for the Market

- Base and peak electricity prices at key hubs.

- Availability of generation (repairs, fuel limitations, network bottlenecks).

- Risk of temporary support measures/limitations introduced by regulators in various countries.

Renewables and Energy Transition: Accelerating Agenda Amid Price Shocks

High oil and gas prices traditionally redirect focus towards renewables, storage solutions, and grid modernisation: the political demand for energy independence is increasing, and long-term investors have strong arguments for accelerating projects. However, in the short term, the market is confronted with the reality that renewables do not always replace gas “in time and scale” without developed networks and storage systems.

- Increased interest in long-term contracts (PPAs) and hybrid solutions “renewables + storage” is anticipated.

- Attention to the supply of critical components and capital costs: raw material and interest rate volatility affects the LCOE of new projects.

For Investors and Energy Market Participants: Scenarios for the Coming Weeks

For the global audience of investors and energy companies, the current market configuration revolves around risk management: the geopolitical premium can rapidly “switch on” and just as quickly disappear, but the consequences through gas, LNG, and petroleum products may be more inertial due to logistics and contractual structures.

Practical Scenario Framework

- De-escalation: rollback of premiums, stabilisation of Brent/WTI, gradually normalising pricing for gas and LNG.

- Prolonged Tension: persistently elevated prices for gas and LNG, costlier supplies of petroleum products, rising freight and insurance.

- Escalation with Physical Disruptions: risk of acute shortages in certain regions, expedited decisions regarding reserves, increased electricity volatility.

Key indicators for tomorrow will remain: news on infrastructure and shipping, price dynamics for oil and gas, physical market premiums for petroleum products, as well as signals from producers regarding their readiness to balance the market. In such an environment, disciplined hedging, diversification of supply chains, and margin control throughout the entire chain—from raw materials to end fuels and electricity—are particularly crucial.