Current News in the Oil, Gas and Energy Sector as of 2 March 2026: Rising Geopolitical Risk Premium on Oil, Supply Risks through the Strait of Hormuz, OPEC+ Dynamics, Gas and LNG Market, Oil Products, Refineries, Electricity and Renewable Energy, Analysis for Investors and Participants in the Global Energy Market

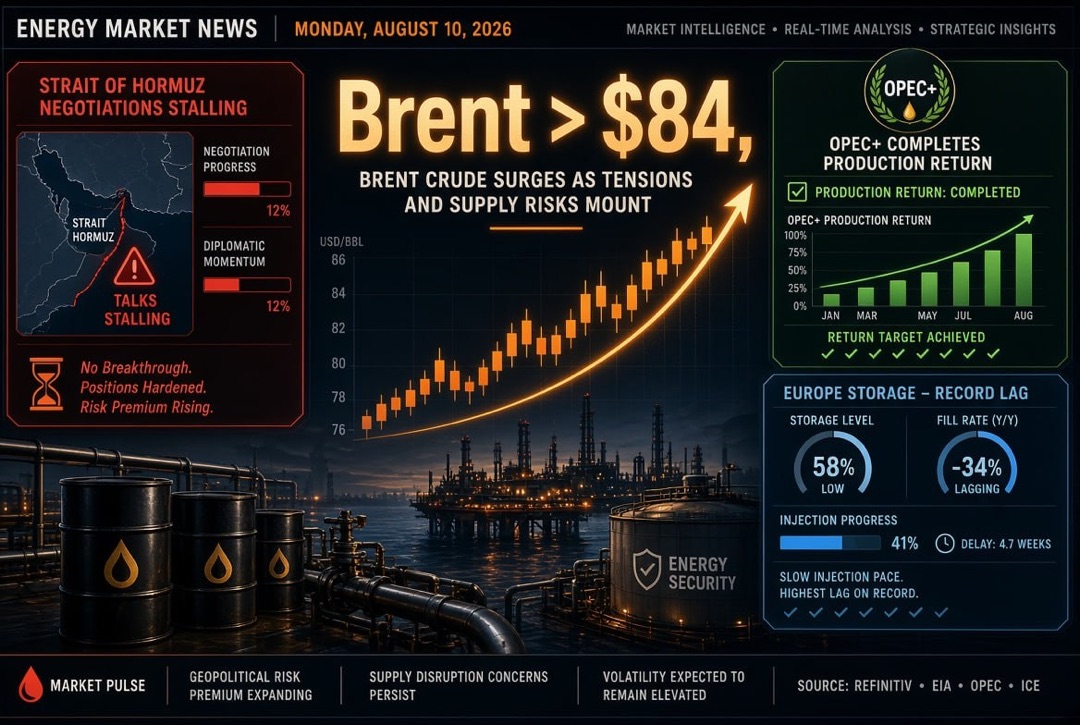

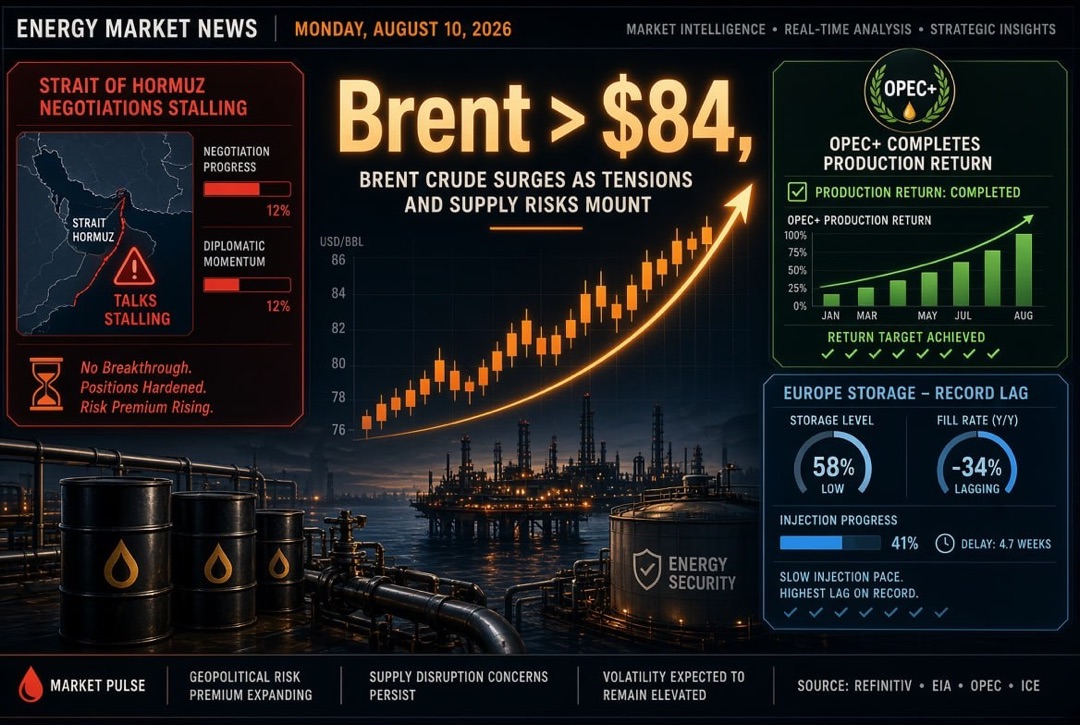

The start of the week for the global fuel and energy sector is marked by a sharp rise in geopolitical risk premiums. Oil and oil products markets are evaluating the likelihood of supply disruptions in the Middle East and their impact on logistics through the Strait of Hormuz, a key route for a significant portion of global maritime oil and condensate trade. Concurrently, the European gas market balances between seasonal demand decline and nerves surrounding LNG supplies, while electricity generation and renewable energy continue to be sensitive to fuel prices and expectations of economic activity.

Key Takeaways for Investors and Market Participants

- Oil: Increased volatility and widening spreads amidst transportation risks; market participants are pricing in scenarios of short-term supply deficits.

- OPEC+: The formally agreed increase in production appears limited compared to the scale of potential shocks; the market is focusing on the actual availability of export routes and reserves.

- Gas and LNG: The European benchmark TTF remains below extreme levels, but the risk premium could surge rapidly if shipping situations worsen and competition for LNG cargo intensifies.

- Oil Products and Refineries: The main channels for transmitting shocks are freight, insurance, transit times and bottlenecks affecting diesel/jet fuel.

- Electricity, Coal, Renewable Energy: Fuel inflation supports 'marginal' generation prices; renewable energy benefits from high gas prices but faces challenges due to network constraints and weather conditions.

Oil: Geopolitical Premium and Supply Disruption Risks

Brent and WTI crude prices are entering a new phase of "event-driven pricing," where short-term news dominates fundamental assessments. Key issues include the safety of maritime transport, the availability of tanker fleets, insurance costs, and the resilience of supply chains for oil, gas condensate, and oil products. For traders and energy companies, this translates into increased margin requirements, a heightened role for hedging, and greater attention to operational flow data.

What This Means in Practice:

- The value of "quick" physical oil and barrels with short logistics (Atlantic/internal supplies) is increasing.

- The likelihood of divergence between raw material prices and refining margins (crack spreads) for individual products is rising.

- There is an increased premium for the quality and availability of grades suitable for specific refineries (especially against the backdrop of medium distillates shortages).

OPEC+: Increased Production is Insufficient if the Issue Lies with Routes and Exports

Market expectations regarding OPEC+'s response are becoming more pragmatic: even if the group agrees to increase production, the market effect depends on whether these additional barrels can physically reach consumers. In a tense environment regarding routes from the Persian Gulf, not only 'spare capacity' but also export infrastructure, terminal availability, and buyers’ willingness to accept crude with heightened logistical risks become key limiting factors.

Focus Areas for Evaluating OPEC+'s Actions Today:

- The actual speed of increasing supplies relative to announced quotas;

- Redistribution of flows in favour of alternative directions and grades;

- Behaviour of strategic reserves (SPR) and commercial stocks at key hubs;

- Signals regarding Saudi Arabia and UAE's readiness to compensate for shocks if they develop further.

Gas and Europe: TTF Pressured by Risks Around LNG and Stock Levels

The European gas market remains relatively stable compared to "crisis" periods but is becoming more vulnerable to news regarding LNG. If shipping risks in the Middle East escalate, the premium could quickly transition from "theoretical" to "monetary"—through increased delivery costs, shifts in routes, and competition between Europe and Asia for spot LNG cargoes.

Key Transmission Mechanism: Even with moderate current TTF quotations, the market is pricing in the likelihood of a "spike" in case access to a portion of global LNG volumes worsens and there is a need for accelerated gas injection into underground storage after winter.

LNG: 2026 as a "Wave of Supply", but Geopolitics Could Disrupt the Balance

From a long-term perspective, 2026 is perceived as a period of accelerated new LNG capacity coming online, easing the global balance. However, in the short term, geopolitical risks could temporarily "overturn" the supply growth effect: spot prices and contract flexibility premiums are rising precisely when logistics become the main constraint.

What Buyers and LNG Traders are Watching:

- Availability of free cargo (spot) and conditions for redirecting shipments (destination flexibility);

- Queues for transit/restrictions in key straits and channels;

- Price differentials between Europe and Asia (TTF vs JKM) as an indicator of flow shifts;

- Utilisation rates of regasification terminals and the state of European stock levels.

Oil Products and Refineries: Diesel, Jet Fuel and Marine Logistics in Focus

For the oil products market, the prices of crude oil (Brent/WTI) are critical, but so are supply chain costs. In the scenario of complicated shipping, products where "transit times" and freight costs constitute a significant portion of the final price—diesel, jet fuel, and bunker fuel—are most responsive. Refineries in Europe and Asia will pay close attention to feedstock availability, stability of component supplies, and margin dynamics.

Practical Implications for the Refining Industry:

- Increased working capital needs for traders and service station networks due to rising oil product stock costs;

- Restructuring of procurement towards nearer sources and contracts with fixed logistics;

- Increased risks of outages and unscheduled refinery repairs become costlier due to the lost margin costs.

Coal and Electricity: Fuel Inflation Sustaining Marginal Generation

Coal remains a backup fuel for various electricity markets, particularly when gas prices rise or become less predictable. As the risk premium on oil and gas increases, so does the likelihood of revising short-term fuel mixes: in certain regions, this will support demand for coal and enhance electricity price volatility (especially in markets with a high share of gas generation).

Renewables: Structural Gains from Expensive Fuels, but Networks and Weather are Key in the Short Term

For renewables (wind, solar), the rise in fossil fuel prices generally boosts relative competitiveness. However, short-term dynamics depend on generation profiles and network constraints: during peak demand and weak renewable generation, the "marginal" source still sets the price. Hence, investors assess not only the "green premium" but also infrastructure—storage, inter-system transfers and network upgrades.

Russia, Sanctions and Shadow Logistics: Where Secondary Effects May Emerge

On the global energy market, the role of "alternative" flows and unconventional logistics solutions increases during periods of stress on traditional routes. For oil and oil products, this means greater attention to fleet, insurance, port infrastructure accessibility, and regulatory risks. Any expansion of restrictions or enforcement could alter discounts, flow directions, and the demand structure for specific oil grades.

What to Monitor on 2 March 2026: Market Checklist

- Brent/WTI Oil: Reaction of the futures curve (backwardation/contango) and premiums for near-term supplies.

- OPEC+: Comments on the actual feasibility of increasing production and export supplies.

- Strait of Hormuz and Freight: Insurance costs, tanker rates, delays and changes in routes.

- Gas TTF and LNG: Spreads Europe-Asia, competition for cargo, rates of withdrawal/injection into underground storage.

- Refineries and Oil Products: Dynamics of crack spreads for diesel and jet fuel, signals on stock levels at hubs.

- Electricity/Coal/Renewables: Sensitivity to fuel prices and weather scenarios in key regions.

The global energy market enters the week with heightened uncertainty, where logistics and risk management become crucial. For investors and participants in the energy sector, priorities remain: controlling exposure to oil volatility, assessing the resilience of gas and LNG supply chains, and understanding how quickly rising raw material prices translate into oil products, electricity and economic activity.