Global Energy News: Oil, Gas, Refined Products and Energy as of 5 March 2026, Key Risk of the Day: The Strait of Hormuz and Global Supply Chain Logistics

The primary driver of the global commodity markets currently is the effective blockage of some flows through the Strait of Hormuz and the sharp increase in logistics costs. In light of the risk of attacks in the Persian Gulf region, tankers and LNG carriers are going 'on standby' – the supply chains for oil, LNG, and refined products are beginning to operate with delays, and the risk premium is shifting from futures curves to freight and insurance. For global energy, this means a rise in prices not only for the raw materials but also for the transport components: VLCC and LNG freight rates are becoming a standalone cost factor for oil companies and trading.

- Freight and insurance – a rapid conduit for transmitting shocks to prices of oil, LNG, and refined products.

- Disruptions in supply schedules enhance the market's price sensitivity to any reports of infrastructural incidents in the region.

- Risk premium is becoming a 'logistics tax' for Asia and Europe: the higher the cost of a barrel, the higher the cost of fuel and electricity for industries.

Oil: Brent and WTI Hover Near Multi-Month Highs

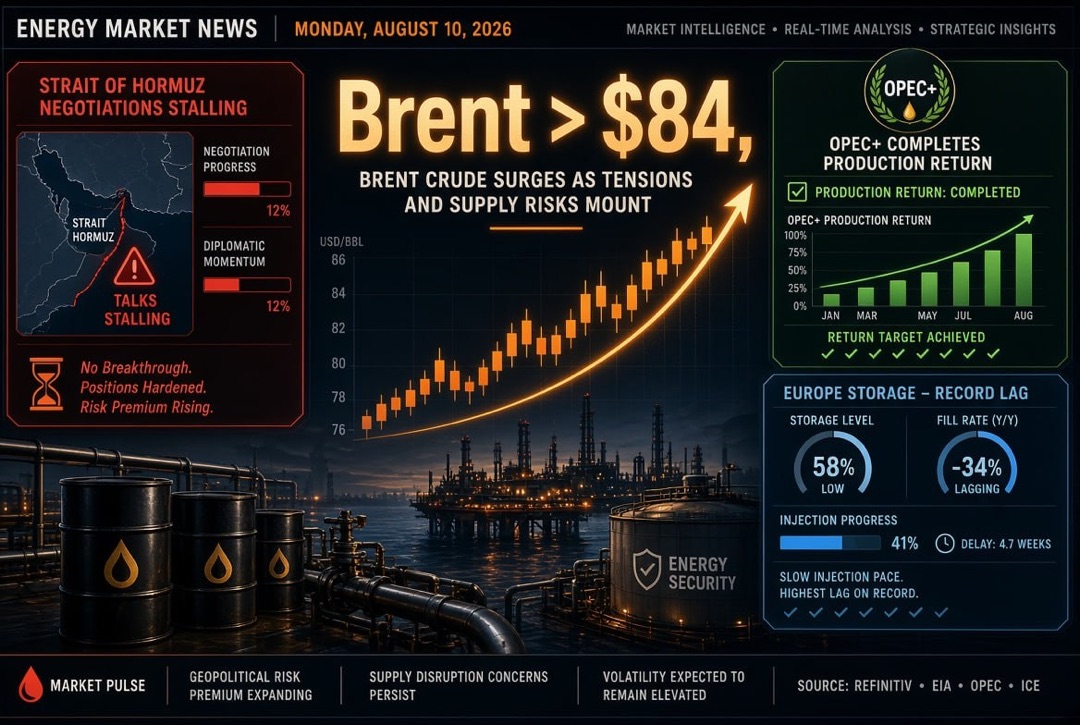

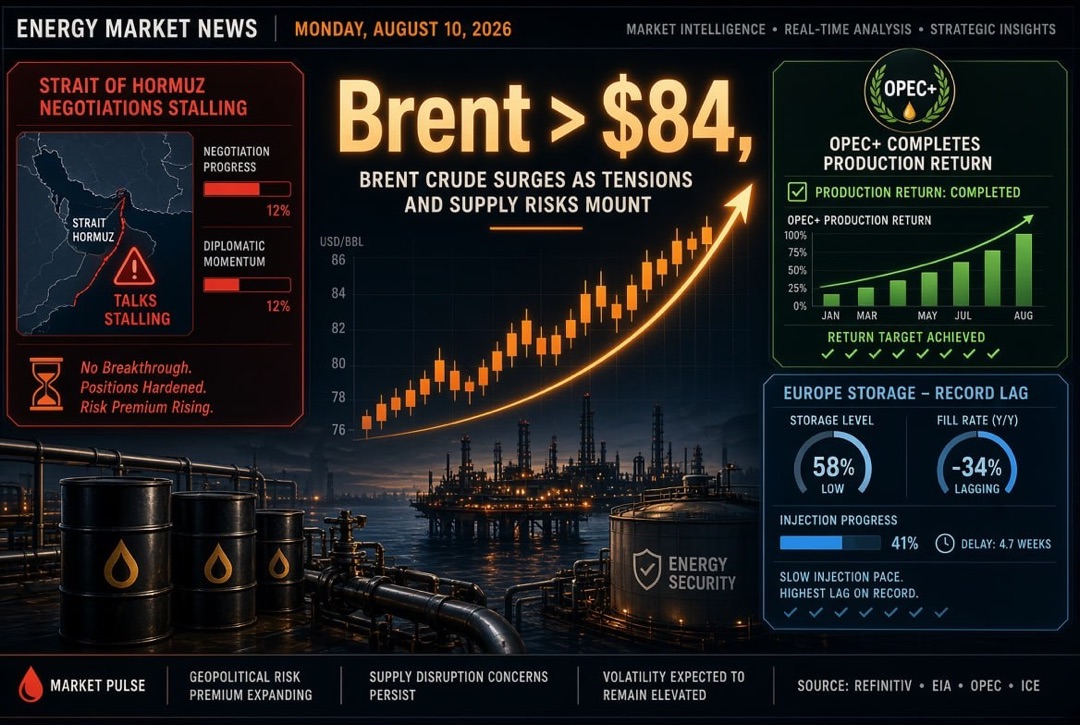

By 5 March, the oil market maintains a nervous tone. Brent remains around $82/barrel after rising to local highs, while WTI hovers near the mid-$70s/barrel. The trigger is a combination of supply disruptions, risks to export infrastructure, and uncertainty regarding the duration of shipping restrictions. In this context, traders are assessing not only 'how much is being produced', but also 'how much is actually reaching' refineries and consumption terminals.

An additional layer is macro data and stocks: an increase in inventories in the U.S. could temporarily smooth out price momentum, but under current conditions, it is perceived as a secondary factor compared to the risks in the Strait of Hormuz and potential production/export stoppages in the Middle East.

- Geopolitics and physical flows (accessibility of the strait, safety of vessels) remain the key drivers for oil.

- Infrastructure risk increases the premium in oil prices and intensifies demand for alternative grades.

- Expectations of de-escalation may provide pullbacks, but the market quickly 'absorbs' any news about the prolonged nature of disruptions.

OPEC+ and Supply: Rising Quotas, but the Market Eyes 'Barrels on Water'

On the supply side, OPEC+ demonstrates a willingness to manage the market, but the Alliance's decisions are currently limited by logistics. Leading participants have agreed to reinstate some voluntary production restraints with a relatively minor increase in output in April – on paper, this appears as a step towards balancing, however, actual delivery is determined by the possibility of exporting and insuring the tanker fleet.

The practical interpretation for investors and oil companies: even with formal increases in production, the 'marginal' factor remains export infrastructure and transport. Therefore, oil largely reacts to news about vessel passages, incidents at production and refining sites, rather than merely the change in quotas.

Gas and LNG: Qatar's Force Majeure Reignites Global Competition for Molecules

The gas and LNG markets are experiencing one of the sharpest stress episodes in recent years. Qatar's force majeure effectively removes the largest flexible source from the market for balancing between Europe and Asia. With a high dependency of some importers on Middle Eastern volumes, a competition 'basin versus basin' arises: Asia is paying more for spot deliveries, while Europe is trying to retain molecules to avoid impairing storage in underground gas storage ahead of the next heating season.

The symptoms are already evident: the European TTF has surged sharply, while the Asian JKM has jumped to levels that reopen arbitrage for deliveries from the Atlantic to Asia. However, physically 'replacing Qatar' is challenging: U.S. LNG exports are already near their peaks, and the short-term reserve in the industry is limited. As a result, the high gas price becomes a global factor for electricity and industrial inflation.

- Europe: risk of high storage costs in underground gas storage and increasing electricity prices in industry.

- Asia: competition for spot cargoes, rising JKM premium, and increased LNG freight costs.

- U.S. and Atlantic: high utilization of LNG export capacities limits the speed of supply response.

Refineries and Refined Products: Diesel and Jet Fuel Outpacing Raw Material Prices

For refined products, the week is characterized by 'bottlenecks': the risk of stoppages at refineries and export terminals in the Persian Gulf, rising freight rates, and changing supply routes exacerbate the shortage of middle distillates. Diesel and jet fuel typically respond first to logistical shocks – they are critical for supply chains, aviation, cargo transportation, and power generation in several countries.

The market exhibits a rapid increase in premiums and spreads: Asian differentials for diesel and aviation fuel are achieving multi-year highs, while the 'East-West' spread for diesel (including forward structures) is intensifying amid expectations that Europe will be forced to draw additional volumes from Asia while restrictions continue through Hormuz. For refineries, this means increasing margins for middle distillates, but at the same time, raised operational risks and volatility concerning raw material procurement and logistics.

- Diesel and jet fuel are in the zone of highest deficit risk given disruptions in Hormuz.

- Refineries and terminals – increased physical risk raises the premium on refined products.

- Europe-Asia – the potential for barrel flow is limited by freight costs and vessel availability.

Electricity and Coal: Gas Shock Intensifies Fuel Switching

High gas prices in Europe and Asia inevitably spill over into electricity prices: in competitive energy systems, gas generation often meets marginal demand and sets the price in the wholesale market. As a result, the spike in TTF and expensive LNG raises the cost of megawatt-hours for industry and stimulates 'fuel switching' wherever possible: there is an increase in demand for coal, fuel oil, and alternative fuels in generation and industrial heat.

Coal receives short-term support in this configuration, as coal indices react with increases. For global energy, this means a temporary strengthening of coal's role and a more complex balance between reliability, price, and climate goals. At the company level, the value of resilient fuel supply chains, access to port infrastructure, and flexibility in the fuel mix is increasing.

Renewables, Hydrogen and Carbon Markets: Energy Security Accelerates Industrial Policy

Alongside the crisis in oil and gas, a long-term outline is gaining weight: countries are enhancing their industrial policies around renewables, batteries, hydrogen, and 'low-carbon' supply chains. In Europe, the discussion of competitiveness and energy prices is reflected in the movement of carbon quotas within EU ETS: the ETS market balances between climate goals and pressure from industries due to the costs of electricity and gas.

Meanwhile, the energy transition trend remains unscathed: the share of wind and solar in several regions continues to grow, and major green hydrogen projects and supply chain localization are receiving political and financial support. For investors, the important takeaway is that by 2026, energy will remain 'two-speed' – short-term shocks support oil, gas, and coal, while structural programmes continue to drive renewables, grids, storage solutions, and hydrogen.

Investor Focus: Scenarios and What to Monitor in the Next 24 Hours

For the energy sector market, the key question for the next day is one – the duration of shipping restrictions and the speed of export normalisation. This not only affects oil and gas but also refined products, electricity, coal, inflation expectations, and regulatory behaviour.

- Traffic and security in the Strait of Hormuz: any signs of regained vessel passages or, conversely, new incidents.

- LNG balance: signals regarding the timing of restoration of Qatari supplies and the scale of actual volume 'losses.'

- European gas: dynamics of TTF and discussions surrounding the pace of injections into underground gas storage against the backdrop of expensive gas.

- Refineries and refined products: premiums on diesel/jet fuel, 'East-West' spreads, vessel availability, and the speed of route readjustment.

- Macro effects: inflation sensitivity regarding oil and gas and possible regulatory reactions to rising energy costs.